© 2024 The Asclepius Initiative Inc. All Rights Reserved

Medicare is a federal health insurance program in the U.S. for people age 65 and older, as well as some younger individuals with disabilities or certain medical conditions.

Medicare is complicated, and there are two main options for coverage: Traditional (also known as Original) Medicare and Medicare Advantage. They are administered and structured in very different ways, affecting which providers recipients can see, how care is approved, and how much they pay out of pocket.

Traditional Medicare

Traditional, or Original, Medicare is run by the federal government. It is made up of separate parts that cover different types of care.

Medicare Part A covers inpatient hospital stays, skilled nursing facility care, hospice care, and some home health services. Most people do not pay a monthly premium for Part A if they have worked and paid Medicare taxes for at least 10 years. However, there is a deductible for each benefit period (such as inpatient hospitalization), and additional daily costs can apply for longer hospital stays.

Medicare Part B covers outpatient care, including doctor visits, preventive services, lab work, and medical equipment. Part B requires a base monthly premium, which is adjusted upward for higher incomes. There is also an annual Part B deductible. After the deductible is met, beneficiaries are typically responsible for 20% of the allowable cost of services, with no limit on total out-of-pocket spending. Penalties may apply for late enrollment.

Medicare Part D provides prescription drug coverage through private plans approved by Medicare. Costs and covered medications vary by plan. Part D includes an annual out-of-pocket maximum. In 2026, this limit is $2,100. This sets a cap on how much will be paid for covered prescription drugs each year. Late enrollment penalties may apply if drug coverage is delayed without other qualifying coverage.

Under Traditional Medicare, the federal government pays providers directly for covered services. Beneficiaries can see any provider nationwide who accepts Medicare, without needing referrals and with limited use of prior authorization.

Because there is no annual out-of-pocket maximum, many people purchase a Medigap policy to help cover deductibles, coinsurance, and other remaining costs. Medigap policies are most accessible and least expensive when purchased at the time of initial Medicare eligibility, when coverage cannot be denied or priced higher due to health conditions.

Medicare Advantage

Medicare Advantage, also known as Part C, is offered by private health insurance companies.

Instead of paying providers directly, Medicare pays a fixed amount per enrollee per month to the insurance company. The plan then determines what and where care is delivered, and how providers are paid.

Medicare Advantage programs combine Part A, Part B, and often Part D into a single plan. Many plans also include additional benefits, such as dental, vision, hearing, and other supplemental services.

Most Medicare Advantage plans use provider networks, which means care is typically limited to certain doctors, hospitals, and health systems within a defined service area. Care outside the network may not be covered except in emergencies, which can be a challenge for those who travel or spend extended time in multiple locations.

These plans often require prior authorization for certain services, meaning the plan must approve care in advance. This can affect when and whether services are received.

Medicare Advantage plans include an annual out-of-pocket maximum, which limits total spending for covered services in a given year. However, costs such as copays and coinsurance can still add up, depending on how often care is needed. Plan details, including costs, benefits, and provider networks, can also change from year to year.

Key Differences in Access and Cost

Traditional Medicare offers broader access to providers and fewer restrictions on care. It allows beneficiaries to receive care nationwide, generally without prior authorization requirements. However, it does not limit total out-of-pocket costs, which can create greater financial risk for those who forgo supplemental coverage.

Medicare Advantage plans offer bundled coverage and include a cap on annual out-of-pocket spending. They may have lower monthly premiums and include additional benefits. At the same time, they often limit provider access, require approvals for care, and restrict coverage to specific providers or geographic areas.

Tradeoffs to Consider

Traditional Medicare provides flexibility in how care is accessed and where it can be received, but often requires additional coverage to manage out-of-pocket costs.

Medicare Advantage may offer lower upfront costs and additional benefits, but it also introduces more rules, limitations, and variability in how care is delivered.

Each comes with requirements and tradeoffs that can affect both access to care and total spending.

Enrollment and Plan Changes

The decision to opt for Traditional Medicare or Medicare Advantage is not permanent, but changes can only be made during specific enrollment periods.

Medicare Open Enrollment (October 15th through December 7th) is the primary period for making changes. During this time, individuals can switch from Traditional Medicare to Medicare Advantage, switch from Medicare Advantage to Traditional Medicare, or change between Medicare Advantage plans. Changes made during this period take effect on January 1st.

Medicare Advantage Open Enrollment (January 1st through March 31st) is more limited. It applies only to individuals who are already enrolled in a Medicare Advantage plan. During this period, they can switch to a different Medicare Advantage plan or return to Traditional Medicare. However, individuals with Traditional Medicare typically cannot use this period to switch from Traditional Medicare to Medicare Advantage.

Timing also matters when someone is first eligible for Medicare. During the Initial Enrollment Period, which begins three months before eligibility and continues for three months after, individuals can choose either Traditional Medicare or Medicare Advantage. After this period ends, options for switching become more limited, and any switch must follow the enrollment periods described above.

If someone switches from Medicare Advantage to Traditional Medicare and wants to purchase a Medigap policy, eligibility and premium costs may depend on health status if they are outside their initial enrollment window. This means coverage may cost more or may not be available.

Traditional Medicare and Medicare Advantage plans have distinct pros and cons. While traditional Medicare has more flexibility and broad access to providers, Medicare Advantage plans offer integrated coverage and potential cost savings through managed care arrangements.

When choosing between traditional Medicare and Medicare Advantage, individuals should consider their health care needs, financial circumstances, and preferences. This can help inform the decision that best fits their situation.

Watch for Medicare Scams and Deceptive Marketing

Medicare is a large program, and scammers may try to take advantage of people who use it. Some cons are meant to steal personal information. Others are used to bill Medicare for services or supplies that were not needed, not requested, or never provided.

Medical identity theft can create serious problems. It can affect Medicare records, lead to incorrect bills, and make it harder to fix coverage or claims issues later.

People who have Medicare should be careful with any unexpected call, mailing, email, text message, or visit that asks for personal information, Medicare numbers, or money. Read information carefully and do not click on any suspicious links or links that are not from a trusted source.

Protect Medicare Numbers

A Medicare number is valuable and should be protected. Medicare cards now use a Medicare Beneficiary Identifier, or MBI, instead of a Social Security number. This change was made to help reduce identity theft and fraud.

Those intending harm may still try to get this number. They may call and say that Medicare is sending a new plastic card, chip card, or metal card. They may claim the Medicare recipient’s current card needs to be verified right away, or that coverage could be canceled.

Medicare does not issue plastic, chip, or metal cards. Medicare cards are paper, and they are free. Medicare also does not call unexpectedly to ask for a Medicare number.

Be Careful With “Free” Medical Equipment Offers

Offers for “free” medical equipment should be viewed with caution. Fraudulent actors may offer back braces, knee braces, diabetic supplies, testing kits, or other medical equipment at no cost. They may say they only need a Medicare number to place the order.

In some cases, the goal is to use that Medicare number to bill Medicare for equipment that was not needed, not requested, or never received. This type of fraud can also affect a person’s Medicare records and future access to health care or supplies.

A person should not give a Medicare number to anyone who calls, visits, or sends a message unexpectedly offering free medical equipment.

Watch for Scams in Long-Term Care Settings

People who live in long-term care facilities may also be targeted. Scams may include unauthorized credit card purchases or bills sent to Medicare for services that were not needed or did not happen.

In some cases, Medicare may be billed for services provided by people who were not properly licensed or qualified. Family members, caregivers, and trusted representatives can help by reviewing Medicare notices, bills, and account statements for anything that looks wrong.

Be Aware of Spoofed Phone Calls

Scammers may use caller ID to make it look like Medicare, the government, or another official agency is calling. This is called spoofing, or vishing (voice phishing.)

The caller may say Medicare coverage is about to be canceled or that the person is owed a refund because of a billing error. Then the caller may ask for a Medicare number, banking information, credit card number, or other personal details.

Medicare does not call unexpectedly to demand personal or financial information. Medicare employees will not threaten to cancel coverage, demand money over the phone, or call to sell a product.

If a call comes unexpectedly and asks for personal information or money, hang up. Then call Medicare directly at 1-800-MEDICARE or go to Medicare.gov for trusted information.

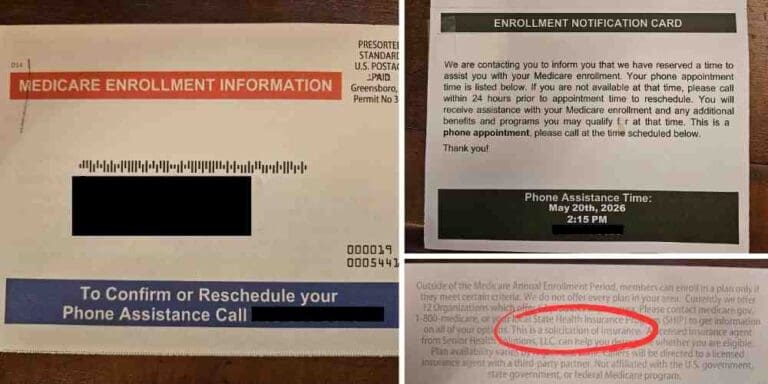

Look Closely at Mail That Looks Official

Some private companies use mailers that look like official Medicare notices. These communications may use red, white, and blue colors, government-style designs, or words such as “Official Medicare Record.” The goal is to make the mailing look like it came from the federal government.

Some correspondence asks people to respond quickly to “secure benefits” or “confirm information.” In reality, the mailing may be from a private company trying to collect contact information or sell a Medicare Advantage, Medicare Supplement, or prescription drug plan.

Read the fine print carefully. If the mailing is from a private insurance company, broker, or sales organization, it is not an official notice from Medicare or the Centers for Medicare and Medicaid Services.

Private companies are not allowed to use words, logos, or designs that falsely suggest they are connected to or approved by Medicare, but many can be easily mistaken nonetheless.

How to Help Prevent Medicare Fraud

People with Medicare can take steps to protect themselves from fraud and deceptive marketing.

A Medicare card should be treated like a credit card. Recipients should not share their Medicare number with anyone who calls, visits, emails, or sends a message unexpectedly.

Medicare Summary Notices and Explanations of Benefits should be reviewed carefully. These documents can show whether Medicare or a plan was billed for services, supplies, or equipment. If something was billed that was not received, it may be a sign of fraud.

Monthly bills for Medicare Part B and Part D premiums should also be checked to make sure the amounts are correct.

Suspicious activity should be reported right away by calling 1-800-MEDICARE, or 1-800-633-4227.

For a more in-depth look at Medicare and Medicare Advantage, click here to watch our webinar.

These materials were supported by funds made available by the Kentucky Department for Public Health’s Office of Population Health from the Centers for Disease Control and Prevention, National Center for STLT Public Health Infrastructure and Workforce, under RFA-OT21-2103.

The contents of these materials are those of the authors and do not necessarily represent the official position of or endorsement by the Kentucky Department for Public Health or the Centers for Disease Control and Prevention.